China has initially established a policy framework for a green financial system, and the participants in the green finance market are becoming increasingly diverse. However, green finance in China remains in a long-term developmental phase. Over years of market practice, several key issues have persisted, including limited information exchange channels, high costs of green asset identification, low data integrity, and weak financial risk prevention mechanisms. The emergence of Green FinTech offers potential solutions to these challenges. By leveraging technological innovation, Green FinTech can enhance various green finance application scenarios and support the broader transition toward a green and low-carbon society.

I. The Concept of Green FinTech

In September 2018, the United Nations Environment Programme (UNEP) introduced the concept of Green Digital Finance (GDF) in its GDF report, defining it as a form of financial innovation enabled by technologies such as Big Data, Machine Learning, Artificial Intelligence, Mobile Technology, Blockchain, and the Internet of Things. These technologies are applied to support environmentally beneficial projects in their investment and financing activities, with the aim of advancing the Sustainable Development Goals (SDGs) [1]. This definition is rooted in the Financial Stability Board’s (FSB) broader concept of “technological innovation in financial services” [2]. When these technological innovations are specifically applied within the realm of green finance, the result is Green FinTech.

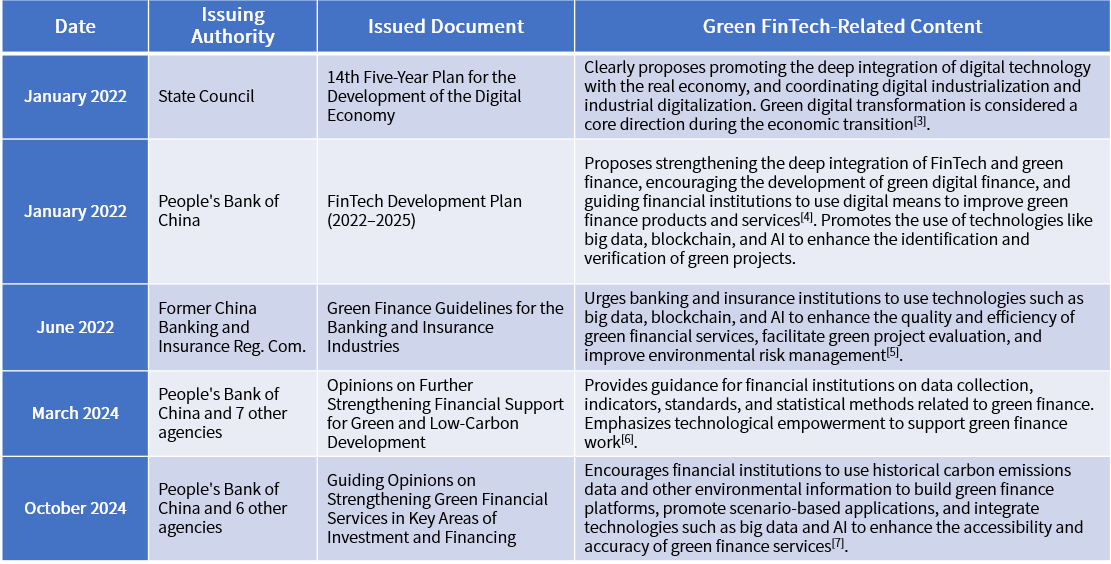

II. Policy Support for Green FinTech

The development of green finance in China has generally followed a dual-track approach, combining effective “top-down” policy-driven initiatives with “bottom-up” reform and innovation, working in synergy to drive progress. In recent years, as the application of financial technology in green finance has expanded, Green FinTech has been increasingly incorporated into the formulation of green finance policy frameworks (see Table 1).

As an emerging field, Green FinTech has only been developing for a few years, yet the spirit of technological innovation has already been embedded in the evolution of green finance in China. To support the national goals of peaking carbon emissions and achieving carbon neutrality, green finance must leverage financial technologies to promote the standardized, integrated development of green finance and FinTech.

Table 1 – Policy Support for Green FinTech

III. The Functions and Roles of Green FinTech

(1) Sustainable Investment Decisions

Faced with vast and complex data sets, Green FinTech can play a unique role. For structured data, big data platforms can be leveraged to clean and mine data related to green finance assets, effectively enhancing the scale, coverage, and timeliness of such data. For unstructured data (such as text, images, etc.), artificial intelligence can be used for image and language recognition, transforming it into usable data. This helps bridge the digital divide people encounter when accessing and using information services, providing technical support for financial institutions in areas such as product innovation, risk control, product pricing, and information disclosure.

(2) Diversification of Investment and Financing Methods

Green FinTech provides technological support for promoting the diversification of investment and financing methods. It can precisely identify the investment preferences on the supply side of funds and the actual needs on the demand side, configuring different financial services according to the characteristics of different industries and property rights. Local governments can establish information connection platforms between Green FinTech and green projects, achieving effective integration and information sharing of green financing data across multiple channels[8].

(3) Deepening the Integration of Industry and Finance

Green FinTech can facilitate the integration of green development and industrial transformation, guiding financial institutions to standardize the provision of financial services in supply chain scenarios[9]. By collaborating with inclusive finance, it can establish green credit standards with local characteristics and environmental impact measurement systems, deepening the integration of industry and finance, and promoting high-quality industrial development.

(4) Greening Production and Life

In production, the Internet of Things technology can be used to monitor corporate carbon emissions data in real-time, promote the construction of digital infrastructure, and drive the precise and efficient implementation of Green FinTech initiatives. In daily life, Green FinTech can connect banking and transportation platforms, extending digital carbon reduction scenarios to various aspects of public life, including clothing, food, housing, and transportation, while offering corresponding incentives to guide the public in adopting low-carbon behaviors.

IV. Typical Cases of Green FinTech

Since 2020, the Paulson Institute Green Finance Center and the Beijing Green Finance & Sustainable Development Research Institute have been closely monitoring the latest policies, market changes, and typical cases related to the role of FinTech in empowering the development of green finance in China. They have reviewed the market trends in the past three years where FinTech supported green finance, resulting in the report "FinTech Driving the Development of Green Finance in China: Cases and Outlook (2023)"[10] (hereinafter referred to as "this report"). Below, we will sequentially share three typical cases of FinTech empowering green finance at the government, corporate, and financial institution levels as presented in this report.

(1) Government-Level Application Scenario: Huzhou Financing Entities ESG Evaluation System

Since its launch in October 2021, the Huzhou Financing Entities ESG Evaluation System has automated, fully implemented, and added value to the ESG evaluation of financing entities, driving innovation in green finance reform in Huzhou. The system takes into account the local industrial structure, the current state of data from different industries, and the differences in ESG business characteristics, dividing the sectors into five industries, with each industry further categorized into large, medium, and small enterprises.

As of now, the system has been upgraded to version 5.0, integrating regional development practices and the shift from "energy consumption dual control" to "carbon emission dual control." It highlights the "dual carbon" goals in the environmental dimension, introduces "carbon account" data, and quantitatively assesses corporate carbon emissions and sensitivity. To date, Huzhou has conducted ESG evaluations for 22,000 enterprises and provided interest subsidies of 76.31 million yuan for 873 green enterprises[11].

(2) Corporate-Level Application Scenario: China Huadian Group Carbon Emission Management Information System

China Huadian Group (hereinafter referred to as China Huadian) is one of the five major state-owned electric power groups directly managed by the central government. Currently, over 100 of its thermal power companies have been included in the national carbon emission trading market, with a carbon quota asset scale exceeding 10 billion yuan.

China Huadian has established a carbon emission management information system based on real-time data. The system covers five key functions: real-time tracking of carbon quotas, MRV (Monitoring, Reporting, and Verification) management of carbon emissions, carbon trading compliance management, carbon financial derivative business management, and the coordinated monitoring of pollution reduction and carbon reduction. This system enables fast compliance with quota obligations and precise carbon asset management.

In 2023, all of China Huadian's key emission units completed their compliance work in just 39 days, becoming the first central state-owned power enterprise to achieve 100% compliance for three consecutive years[12]. In 2023, the carbon dioxide emissions per 10,000 yuan of output value decreased by 3.37% year-on-year, and compared to 2020, it decreased by 17.07%. The comprehensive energy consumption per 10,000 yuan of output value decreased by 12.3% compared to 2020, showing a significant reduction in the economic "carbon intensity[13]."

(3) Financial Institution-Level Application Scenario: China Ping An CN-ESG Smart Evaluation System

In investment evaluation and risk control, China Ping An relies on the CN-ESG Smart Evaluation System and provides intelligent tools and data support for ESG risk control, model construction, and portfolio management through the AI-ESG platform. Using this evaluation model system, Ping An conducts ESG due diligence on listed companies, bond issuers, and projects, which serves as the evaluation standard and basis for investment and asset risk management.

The AI-ESG platform utilizes technologies such as OCR for report image analysis, natural language understanding, remote sensing image analysis, and knowledge graph big data analysis to automate and multi-channel collect and analyze various data sources. The data covers 3,900 A-share listed companies, with more than 350 data points per company. By leveraging diversified local data and alternative data sources, the platform performs in-depth cleaning and validity verification to enhance the completeness, timeliness, and accuracy of the underlying data, thus realizing AI empowerment.